I've been on OnlyFans long enough to remember when it felt like a niche corner of the internet—before the headlines, before the celebrities, before everyone suddenly became a "creator."

And if there's one thing I've learned after subscribing to hundreds of profiles, building Fanspedia, and tracking this space obsessively, it's this: most of what people think they know about OnlyFans is either outdated, cherry-picked, or straight-up wrong.

The real numbers tell a much more interesting story. So in this guide, I'm breaking down the latest OnlyFans statistics (April 2026)—from revenue and user growth to creator income and traffic patterns—so you can actually understand how this platform works under the hood, not just the hype you see on TikTok.

TL;DR – 10 Key Stats (April 2026)

- ~430M total registered users (April 2026 est.)

- ~5.3M total content creators (April 2026 est.)

- ~$7.95B in fan transactions (full-year 2025)

- ~$29B+ paid to creators since 2016 (extrapolated to April 2026)

- ~80% of users are male (~344M men vs ~86M women)

- ~75% of creators are female (~3.98M women vs ~1.32M men)

- Top 0.1% of creators earn 76% of revenue (average ~$147K/mo) – vast inequality

- Only ~4.5% of users pay anything (implying ~95.5% of users pay nothing)

- 84.1% of visits are mobile (desktop 15.9%) — confirmed Dec 2025

- OnlyFans ranks #93 globally (~300M+ visits, Feb 2026), growing ~+15% YoY

Overview & Key Facts

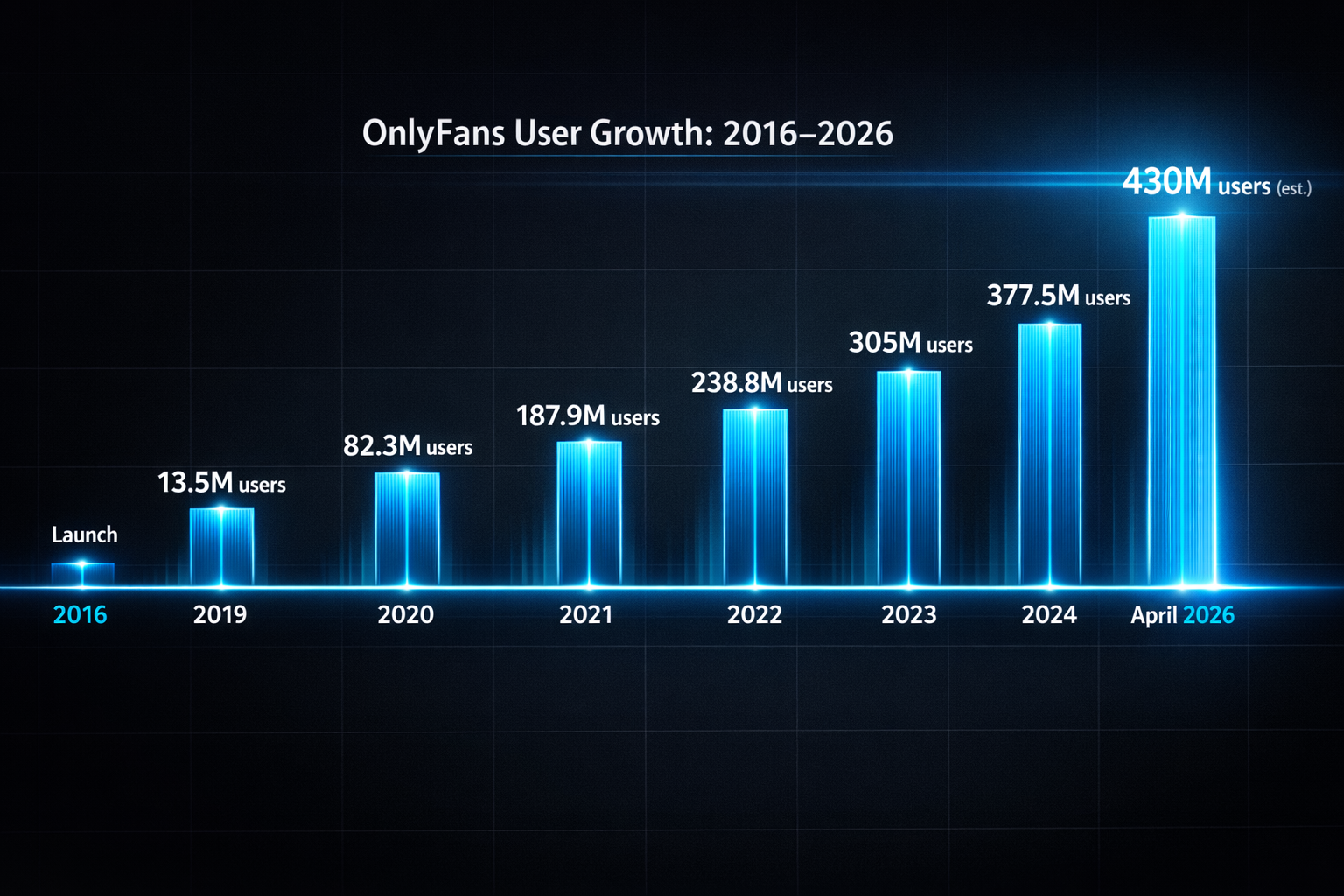

OnlyFans launched in November 2016 and exploded during the pandemic. Today (April 2026) it boasts roughly **430 million user accounts** and **5.3 million creators**. To put that in perspective: it's as if a third of the US population — plus tens of millions more globally — has an OnlyFans account.

The site is truly global: about 50% of traffic is from the U.S., with the UK (6%) and other countries trailing. Unsurprisingly, the US also has ~45% of all creators.

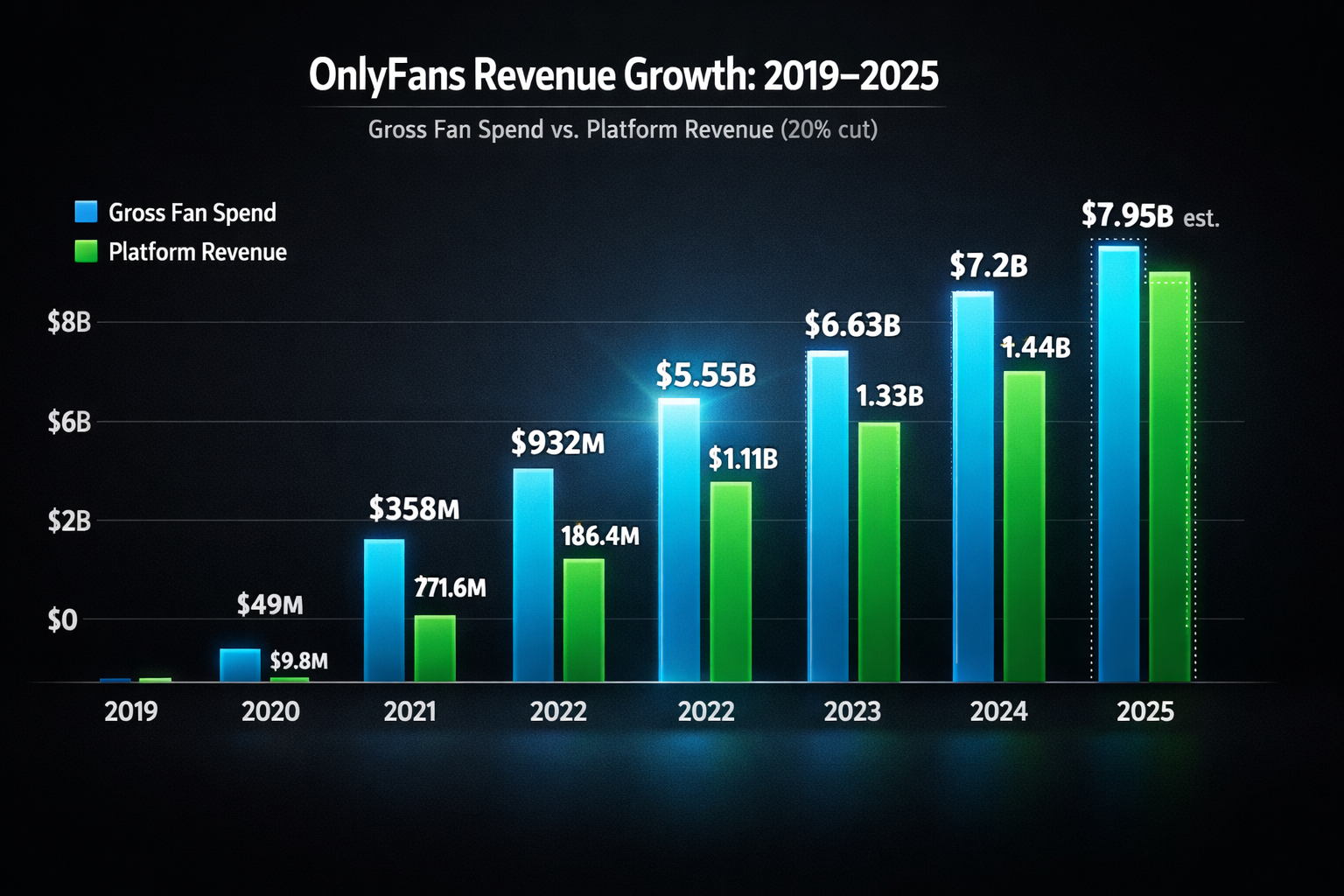

For founders and investors, growth has been remarkable but is now normalizing: users grew ~14% year-over-year in 2025 (moderating from the post-pandemic surge), and creators grew ~15%. The platform's owner (Fenix Int'l) saw fan spend rise from $375M in 2020 to $7.2B in 2024 — a 17x increase in four years.

On the corporate side, an attempted $8B valuation sale fell through in January 2026, and majority owner Leonid Radvinsky died in March 2026 while in talks with Architect Capital at a revised $3.5B valuation — leaving the company's ownership future currently uncertain. (Source: Wikipedia, updated March 2026)

- Total users:~430M (April 2026 est.)

- Total creators: ~5.3M (April 2026 est.)

- Founded: November 2016, London (Tim Stokely)

Key Takeaway: OnlyFans is massive. With hundreds of millions of accounts and millions of creators, it's grown from a niche site to a global content juggernaut in under 10 years. Growth is moderating but the scale is now extraordinary. That sets the context for the deeper dive below.

Revenue & Financials

The money numbers are staggering. In 2025, fans spent an estimated **$7.95 billion** on OnlyFans subscriptions, tips, and pay-per-view content. Since OnlyFans takes a 20% cut, that yielded roughly **$1.59 billion in platform revenue**. For context, year-on-year fan spend growth was +10.4% in 2025 — strong but normalizing from the +19% recorded in 2023. By April 2026, the platform has cumulatively paid creators an estimated **$29 billion+** since launch (confirmed at $25B+ as of October 2025, per official announcement).

Other financial highlights: Fenix Int'l reported ~$658M pre-tax profit for 2023; the 2025 equivalent is estimated to be in a similar range given stable margins. Note: majority owner Leonid Radvinsky, who had personally cashed out significant dividends (including $497M in 2024), died in March 2026. The future ownership structure of Fenix Int'l is currently unresolved. Overall revenue per active user remains high — roughly $18–20 per registered user per year.

- Annual Fan Spend: ~$7.95B in 2025 (+10.4% YoY)

- Platform Revenue: ~$1.59B (2025 est., OnlyFans' 20% cut)

- Growth: Fan spend +19% in 2023, +9% in 2024, +10.4% in 2025 (stabilizing)

- Cumulative creator payouts: ~$29B+ through April 2026

Key Takeaway: OnlyFans has turned into a billion-dollar powerhouse. Yearly fan spending is approaching $8B, and the platform itself takes over $1.5B/year. Growth is moderating but revenue per user remains high — this is now a mature, profitable business, not a hypergrowth startup.

Creator Economy Stats

I've seen this firsthand: most creators make little money, while a few make a fortune. Key stats:

- Active creators: ~5.3M in April 2026 (roughly 81 fans per creator)

- Creator growth: +15% in 2025; +40% in 2023 (pandemic-era peak). Total growth since 2019: ~1,414%

- Top earners: Only a tiny slice cash out: top 0.1% of creators earn ~76% of income

- Average income: Industry sources estimate the average OnlyFans creator earns only $131–$180 per month. In other words, the median creator makes under $2K/year.

- Income concentration: Even the top 10% of creators make 73% of revenue, leaving 90% of creators sharing only 27%

- Income tiers: The top 1% of creators average about $33,984/month (~$408K/year). In practice, only about 53,000 creators (1% of 5.3M) reach that level. The top 0.1% (~5,300 creators) average ~$147K/month. The remaining ~4.77M creators mostly earn in the low hundreds per month — or nothing

- Income share: Top 1% = 33% of income; Top 10% = 73%; Bottom 90% = 27%

- Dependence on few fans: Only ~4.5% of users pay, so only ~19–22M accounts buy anything. This tiny paying crowd funds the entire creator economy

Key Takeaway: The creator economy is a power law: a few superstars earn millions while the vast majority scrape by. In my experience, this means the narrative "anyone can make big money on OnlyFans" is deeply misleading — only elite creators do.

Subscribers & Fan Behavior

In April 2026, we estimate ~430M total registered accounts — but not all are paying. Based on updated estimates, roughly 4.5% of accounts are paying subscribers**, implying approximately **19–22 million paying fans.

Those who do pay spend heavily, averaging around $397/year ($7.95B ÷ ~20M paying fans), or roughly $33/month.

- Total fans: ~430M registered (April 2026 est.); actual paying subscribers ~19–22M (~4.5% of users)

- Avg spend: ~$397/year per paying fan (~$33/month)

- Retention: OnlyFans doesn't publish retention data, but surveys suggest high churn; many fans subscribe for 1–2 months then cycle off

- Non-paying majority: ~95.5% of subscribers spend nothing — a tiny minority of "whales" fund the entire platform

Demographically, most fans are young adult males. Platform analytics confirm that the vast majority of financial activity comes from a core group of highly loyal, repeat-paying subscribers. Creators who retain those buyers long-term are the ones who climb income tiers.

Key Takeaway: Only a small fraction of OnlyFans users pays; that core fan base spends heavily (~$397/year). Real money comes from a tiny percentage of loyal, paying subscribers — meaning creators compete fiercely for those ~20M wallets across 5.3M creator accounts.

Content & Niche Trends

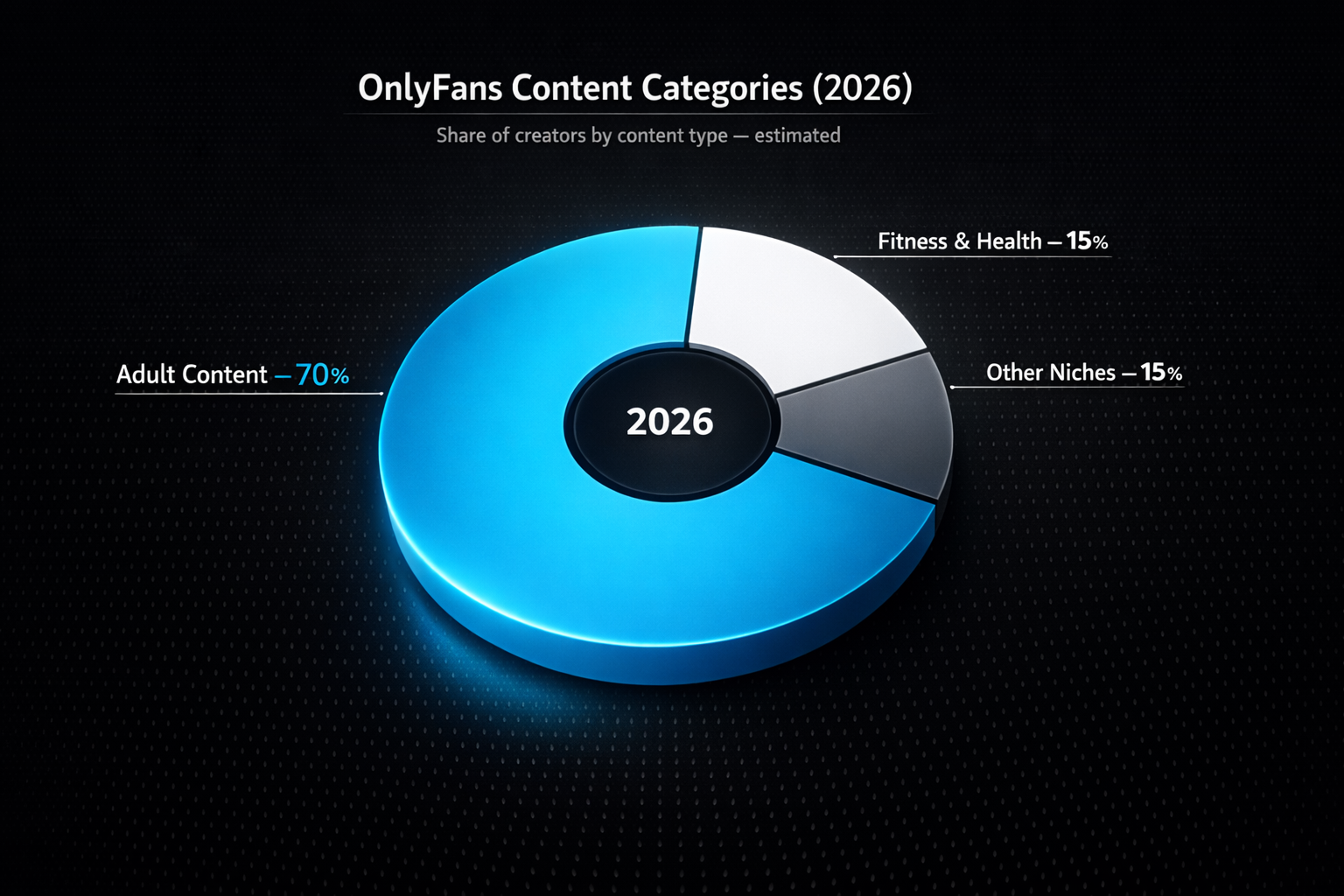

OnlyFans started as an adult platform, and adult content still dominates. Roughly 70% of creators produce sexual or erotic material. The remainder focus on fitness, music, cooking, life coaching, cosplay, and more. The platform even rolled out "OFTV" for sports, fitness, and cooking streams — but non-NSFW creators remain a clear minority.

- Adult content: ~70% of creators

- Fitness/Health: ~15%

- Other niches (music, cooking, lifestyle, education, cosplay): collectively ~15%

The revenue share skews even more toward adult content — top earners are almost exclusively adult content creators. Lifestyle influencers do well but rarely reach the very top income bracket. Female sports and fitness personalities have gained ground in recent years, but they remain far behind the adult core in raw revenue terms.

Key Takeaway: Adult content creators rule OnlyFans. Roughly 7 in 10 creators produce sexual or erotic material. Non-adult niches exist (fitness, music, cooking), but they're much smaller by both count and revenue. OnlyFans is still seen primarily as an adult platform despite ongoing efforts to diversify.

Growth & Traffic

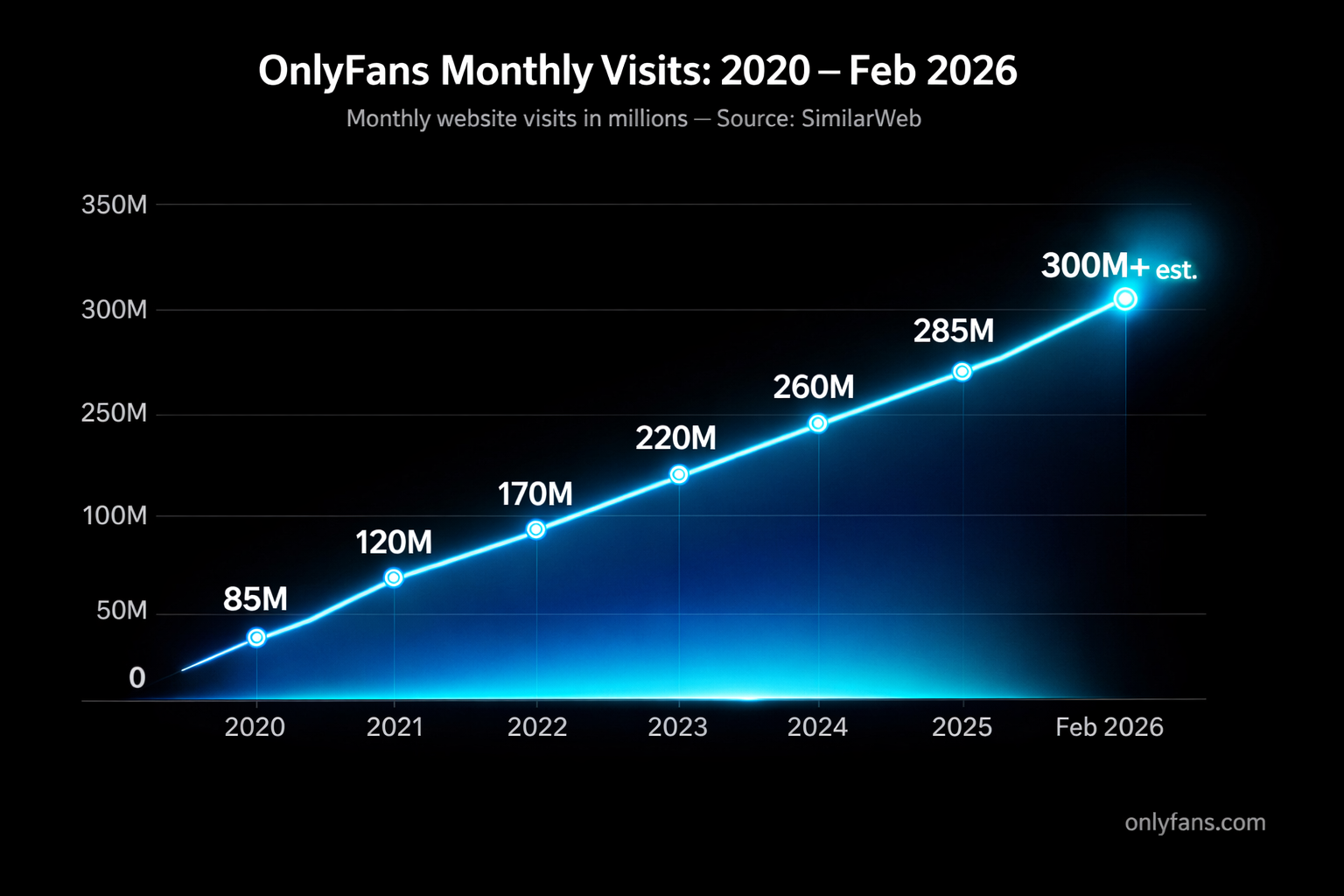

Traffic data shows continuing — if moderating — growth. SimilarWeb ranks OnlyFans at approximately **#93 globally (February 2026) with ~300 million monthly visits, up ~15% year-over-year. Mobile accounts for 84.1% of all visits; desktop just 15.9% — confirmed December 2025 data.

Traffic sources are heavily organic. A breakdown (January 2026) shows: ~55% direct traffic, ~6.7% Google organic, ~4.8% X/Twitter, ~1.9% Instagram. In short, creators rely on Google/SEO and direct links far more than paid social for conversions.

Growth phases:

- 2016–2020: Exponential rise (13.5M → 82.3M users)

- 2021: Peak pandemic growth (120M by March 2021)

- 2022–2024: Strong but decelerating growth

- 2025–2026: Stabilizing at ~13–15% annual traffic growth

Seasonally, holiday months (November–December) are traffic peaks; summer months typically dip.

Key Takeaway: OnlyFans traffic is still climbing — the site now ranks in the top 100 globally. ~58% of traffic comes via search or direct, meaning strong SEO and high-intent users. Social media ads are secondary; real growth comes from discoverability (Google, Reddit, fan networks).

Geographic Distribution

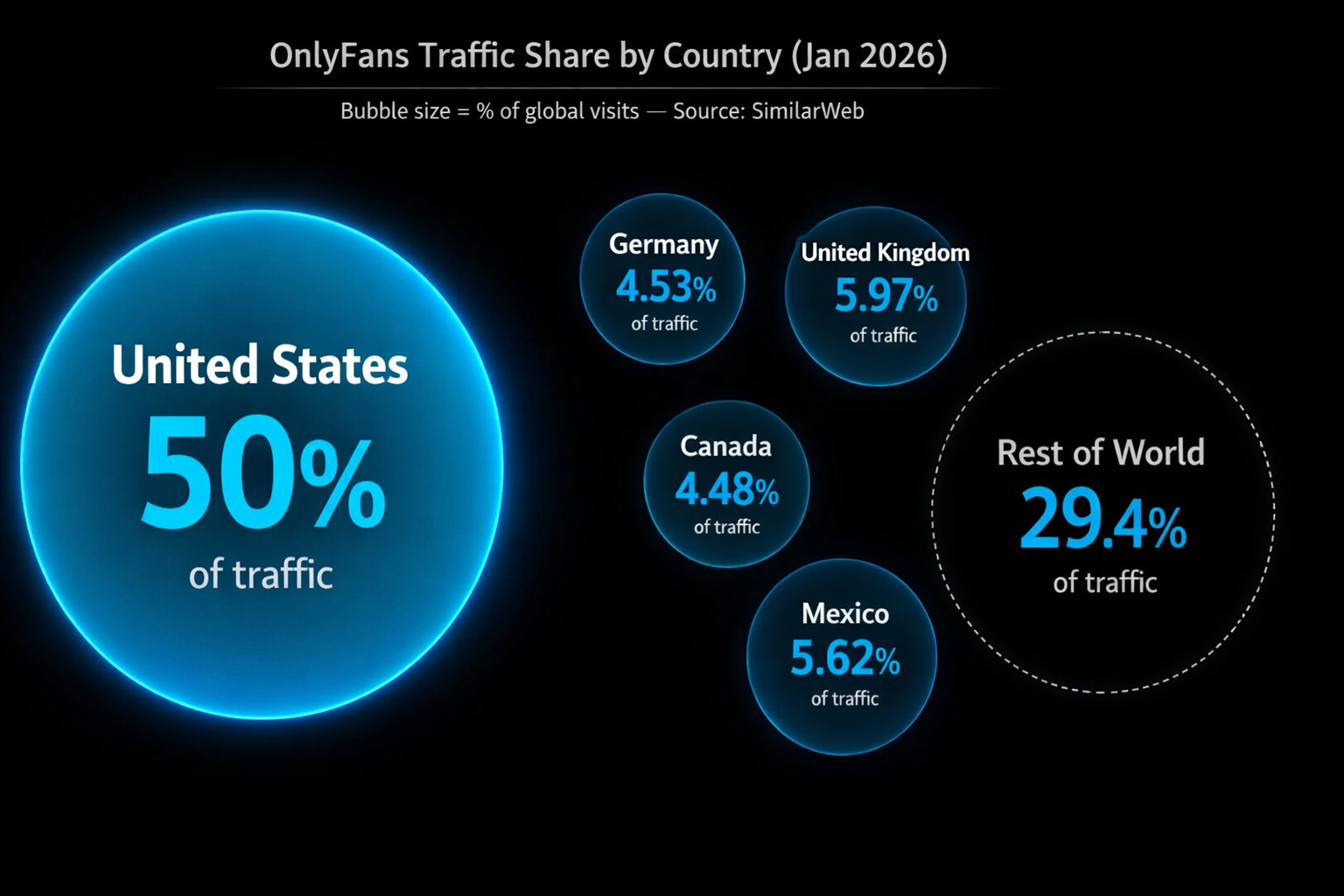

Where are OnlyFans users? The U.S. leads by a wide margin. SimilarWeb traffic share (January 2026): **USA ~50%, UK ~5.97%, Mexico ~5.62%, Germany ~4.53%, Canada ~4.48%**. All other countries each account for less than 4%.

In absolute spending, Americans outpace everyone else dramatically. One 2025 dataset shows US fans spent ~$2.637B vs. $531M in the UK — nearly five times more. Spain and Italy showed the strongest year-over-year growth in fan spend (+24%), signaling rapidly rising activity in Southern Europe.

- User ranking by traffic: US > UK > Mexico > Germany > Canada

- Creator ranking: US (~45%) >> UK (~20%) >> Canada (~10%) >> Australia (~7%)

- Spending: US fans spend approximately 5× more than UK fans in absolute terms

OnlyFans is active in 150+ countries, but usage is concentrated in developed Western markets. Emerging markets (Asia, Africa) remain small due to payment infrastructure and regulatory barriers.

Key Takeaway: OnlyFans is, in practical terms, a US-dominated platform. Half its traffic and nearly half its creators originate from the United States. This shapes content language (English), pricing (USD), and content style.

Social Media & Marketing

How do creators drive traffic? The lion's share comes from outside social media — organic and direct sources dominate. However, social media is where creators build initial followings.

- Traffic sources: ~55% direct, ~6.7% Google organic, ~4.8% X/Twitter, ~1.9% Instagram. Combined, direct + organic = over 85% of all traffic

- Top platforms used by creators: X/Twitter and Instagram (teaser content + OF links); TikTok (massive reach but often removes OF links, creators put links in bio); Reddit (highly conversion-efficient — a single top post can beat a month of TikTok for paid subscribers)

- Social stats: ~80% of creators report using Instagram and TikTok to acquire fans (creator survey). Top creators have millions of IG followers funneling to their OF profiles

- Strategies that work: Community-building (email lists, private Discord/Telegram groups), collaborations, giveaways, and SEO-optimized profile names ("OnlyFans [Name]" Google searches)

Key Takeaway: OnlyFans traffic is largely driven by direct visits and search — but social is where creators grow their initial audience. The biggest mistake new creators make is ignoring SEO and community channels. Only ~7% of traffic comes from mainstream social directly, so diversification (Reddit, SEO, direct fan outreach) is essential.

Platform Comparisons

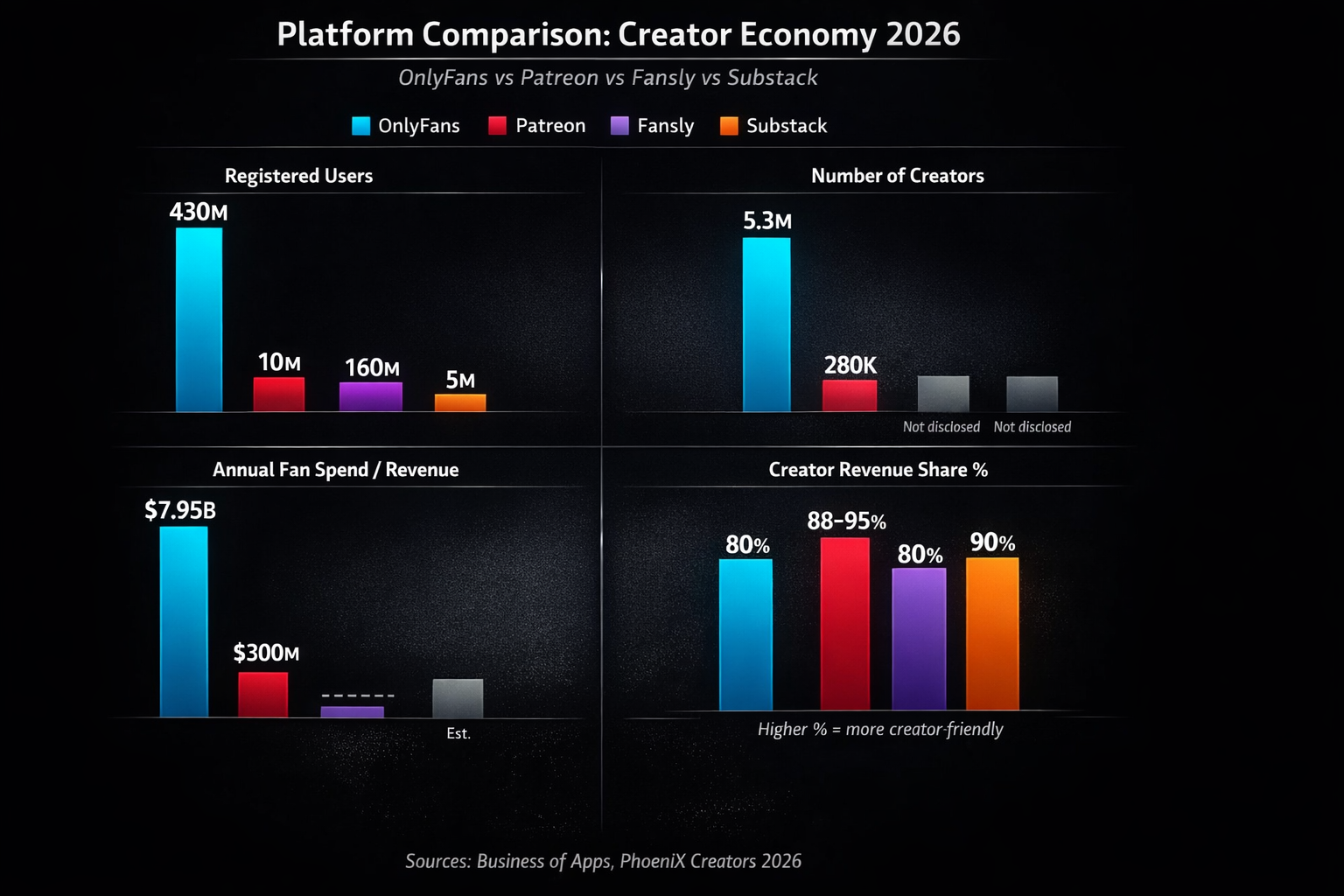

How does OnlyFans stack up against competitors? In short, it dwarfs them all.

| Platform | Users | Creators | Annual Revenue | Creator Cut | | --- | --- | --- | --- | --- | | OnlyFans | ~430M (2026 est.) | ~5.3M | ~$7.95B fan spend | 80% | | Patreon | ~10M paying patrons | ~280K paid | ~$300M creator payouts | 88–95% | | Fansly | ~130–190M (est.) | N/A | Not disclosed | 80% | | Substack | ~5M paid subs | N/A | Smaller scale | 90% |

- Scale gap: OnlyFans processes more in a single month than Patreon pays creators in an entire year. Patreon's annual creator payouts (~$300M) compare to OnlyFans' estimated ~$29B cumulative payout through April 2026

- Business model: OnlyFans and Fansly take 20%. Patreon scales by plan (5–12% + fees). Substack takes 10%. OnlyFans' adult-content moat makes it uniquely defensible — no rival matches its market share there

- Valuation gap: OnlyFans' attempted $8B sale price (January 2026, fell through) dwarfs Patreon's last known valuation of ~$4B

Key Takeaway: OnlyFans is in a league of its own. It has orders of magnitude more users and dollars flowing than Patreon or Substack. This comparison highlights how OnlyFans is the definitive platform for subscription-based creator monetization — especially in adult content.

Future Trends & Projections

The creator economy is booming. A recent report values it at ~$235B in 2026, on track to ~$528B by 2030. OnlyFans, as a dominant player, benefits from that tailwind.

Key projections and developments:

- OnlyFans surpassed **400M registered users by January 2026 (Source: Followchain). Analysts now forecast 500M+ users by 2028**

- 2026 base case: ~$7.95B fan spend, ~$1.59B platform revenue, ~$6.36B paid to creators (Source: PhoeniX Creators, State of OnlyFans 2026)

- The attempted $8B IPO/sale valuation fell through in January 2026. In March 2026, majority owner Leonid Radvinsky died while in acquisition talks at a revised $3.5B valuation — ownership transition is ongoing and creates uncertainty

- OnlyFans is investing in AI chat features, live streaming improvements, and expanded fitness/music verticals (OFTV) to reduce reliance on adult content

- Geographic expansion into Brazil and Southern Europe (Spain, Italy +24% YoY spend) is a clear growth vector

- The post-pandemic surge is over; growth normalizes to **mid-single digits in fan spend** and **high single digits/low double digits in users** going forward

Key Takeaway: The future looks solid but no longer explosive for OnlyFans. With the creator economy surging toward $528B by 2030, OnlyFans has structural tailwinds. The key wild cards are: ownership transition post-Radvinsky, regulatory pressure (UK's Ofcom fined OnlyFans £1.05M in March 2025 for age assurance failures), and whether OFTV can meaningfully diversify the platform beyond adult content.

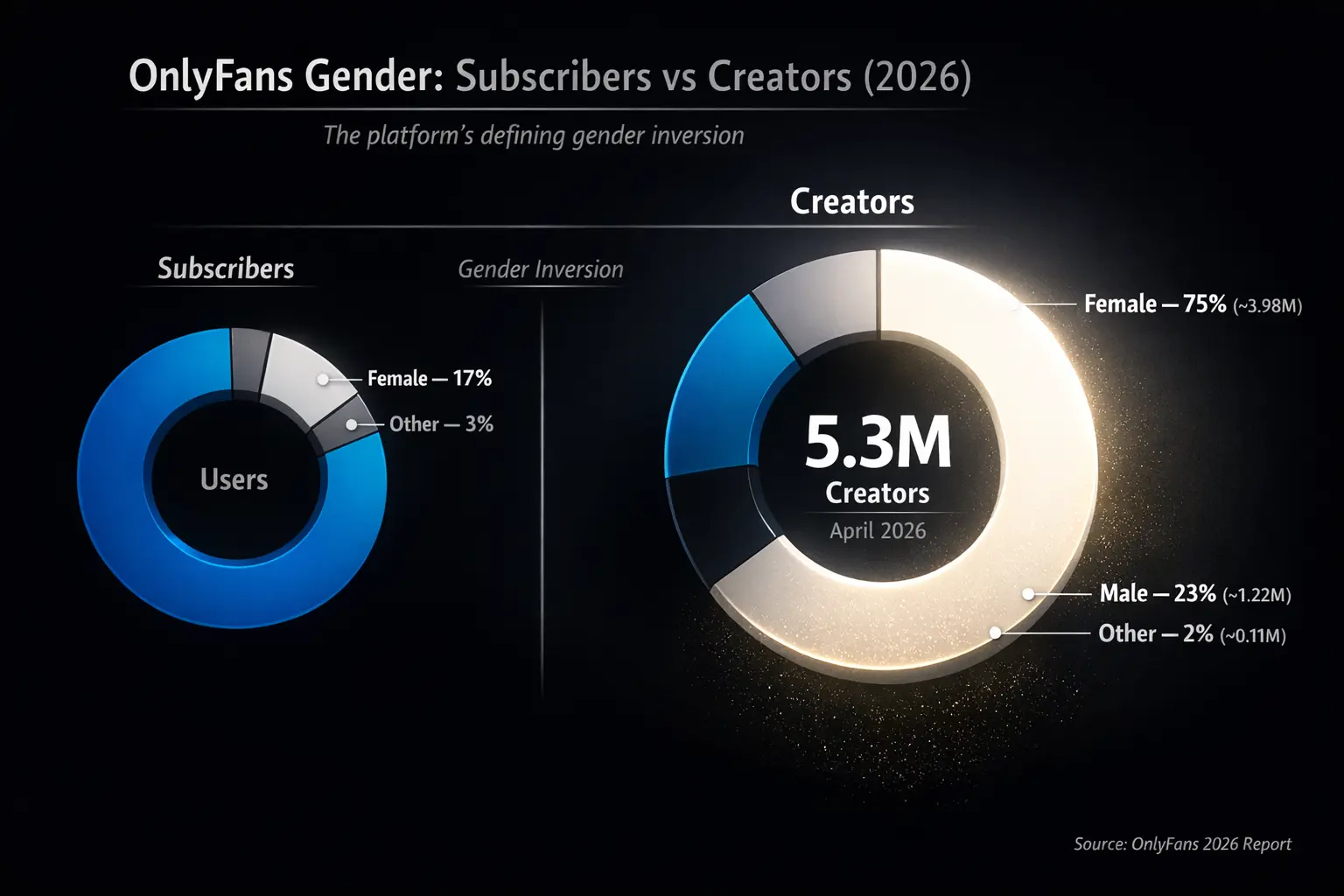

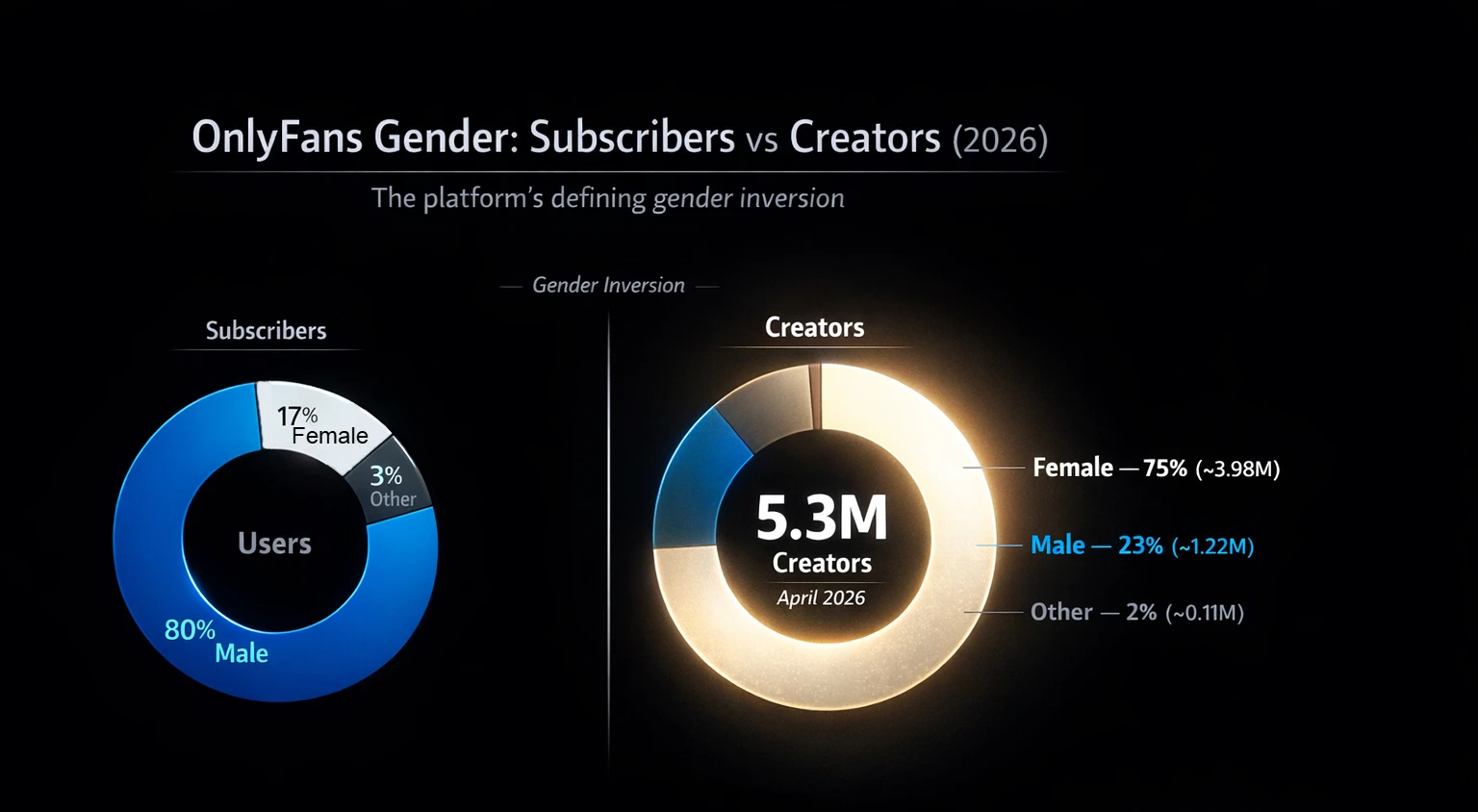

User Gender Demographics

It's well-established: the subscriber base is overwhelmingly male. Multiple sources confirm ~80% of users are male. Taking 80% of 430M estimated April 2026 users, that's approximately 344M male users vs. ~86M female users.

| Gender | Percentage | Estimated Users (April 2026) | | --- | --- | --- | | Male | ~80% | ~344M | | Female | ~17% | ~73M | | Other/Undisclosed | ~3% | ~13M |

This male dominance has major implications: content on OnlyFans is largely created for men. The data aligns with the insight that OnlyFans functions primarily as a male-consumption platform, which in turn explains the female-dominated creator side (see next section).

Key Takeaway: Roughly 4 out of every 5 OnlyFans users are male. This gender skew is one of the most important structural facts about the platform — it explains content trends, creator strategies, and the enormous income potential for female creators targeting that audience.

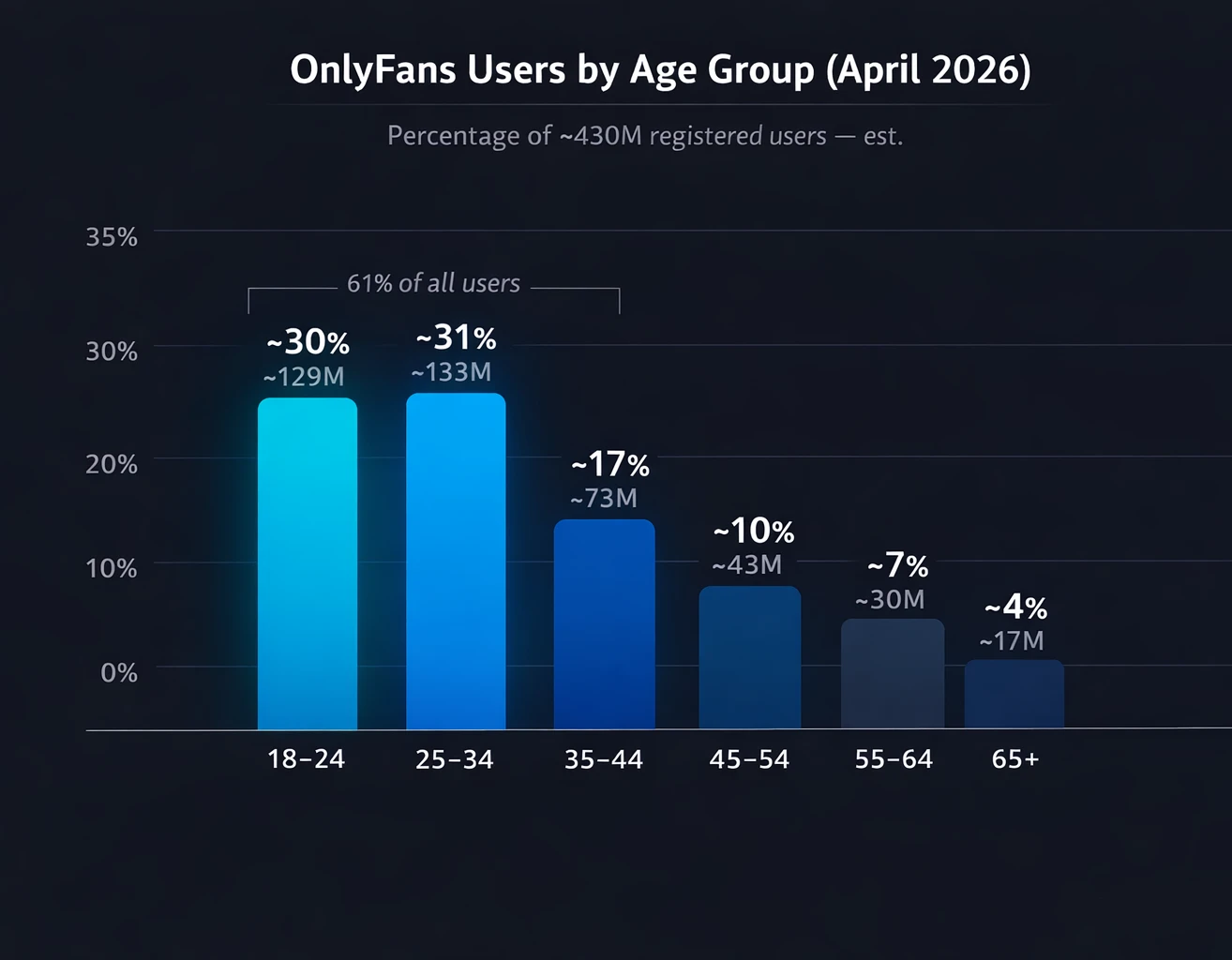

User Age Demographics

OnlyFans users are predominantly young adults. Analytics from SimilarWeb and multiple surveys indicate ~61% of users are under 35. The largest segment, 25–34, makes up approximately 31% of users; 18–24 follows at roughly 30%. The remainder: 35–44 (~17%), 45–54 (~10%), 55–64 (~7%), 65+ (~4%).

| Age Group | Percentage | Estimated Users (April 2026) | | --- | --- | --- | | 18–24 | ~30% | ~129M | | 25–34 | ~31% | ~133M | | 35–44 | ~17% | ~73M | | 45–54 | ~10% | ~43M | | 55–64 | ~7% | ~30M | | 65+ | ~4% | ~17M |

Translating to raw numbers (using 430M): roughly 129M users are 18–24, 133M are 25–34. These two groups alone represent 262M users — over 60% of the entire platform. OnlyFans is, at its core, a millennial and Gen Z platform.

Key Takeaway: OnlyFans is a young-adult platform. If you're a creator targeting new fans or a marketer analyzing the space, aim at 18–34 year-olds — they represent 61% of all users. Usage drops sharply after 45. This matches the heavy social-media promotional strategy creators use, since 18–34s are the most active on TikTok, Instagram, and Reddit.

Creator Gender Demographics

The creator side tells the opposite story from subscribers. Roughly 70–75% of creators are female — some analyses cite as high as 84%. Using a conservative 75% estimate across 5.3M total April 2026 creators:

| Gender | Percentage | Creator Count (April 2026 est.) | | --- | --- | --- | | Female | ~75% | ~3.98M | | Male | ~23% | ~1.22M | | Other/Undisclosed | ~2% | ~0.11M |

This female-majority creator landscape is a key structural insight. On one side, ~344M male fans; on the other, ~3.98M women creators providing the content those fans pay for.

This gender inversion is unique to OnlyFans — on YouTube or Instagram, creator gender is much closer to parity.

- Implication for female creators: Enormous opportunity, but also enormous competition (3.98M women competing for ~20M paying subscribers)

- Implication for male creators: Scarcity creates a niche — specialized male creators (fitness, gay content, male POV) punch above their weight

Key Takeaway: OnlyFans is a female-led creator economy. Roughly 3 out of 4 creators are women, serving a platform that is 4 out of 5 male subscribers. This supply-demand dynamic is the core engine of OnlyFans' entire revenue model.

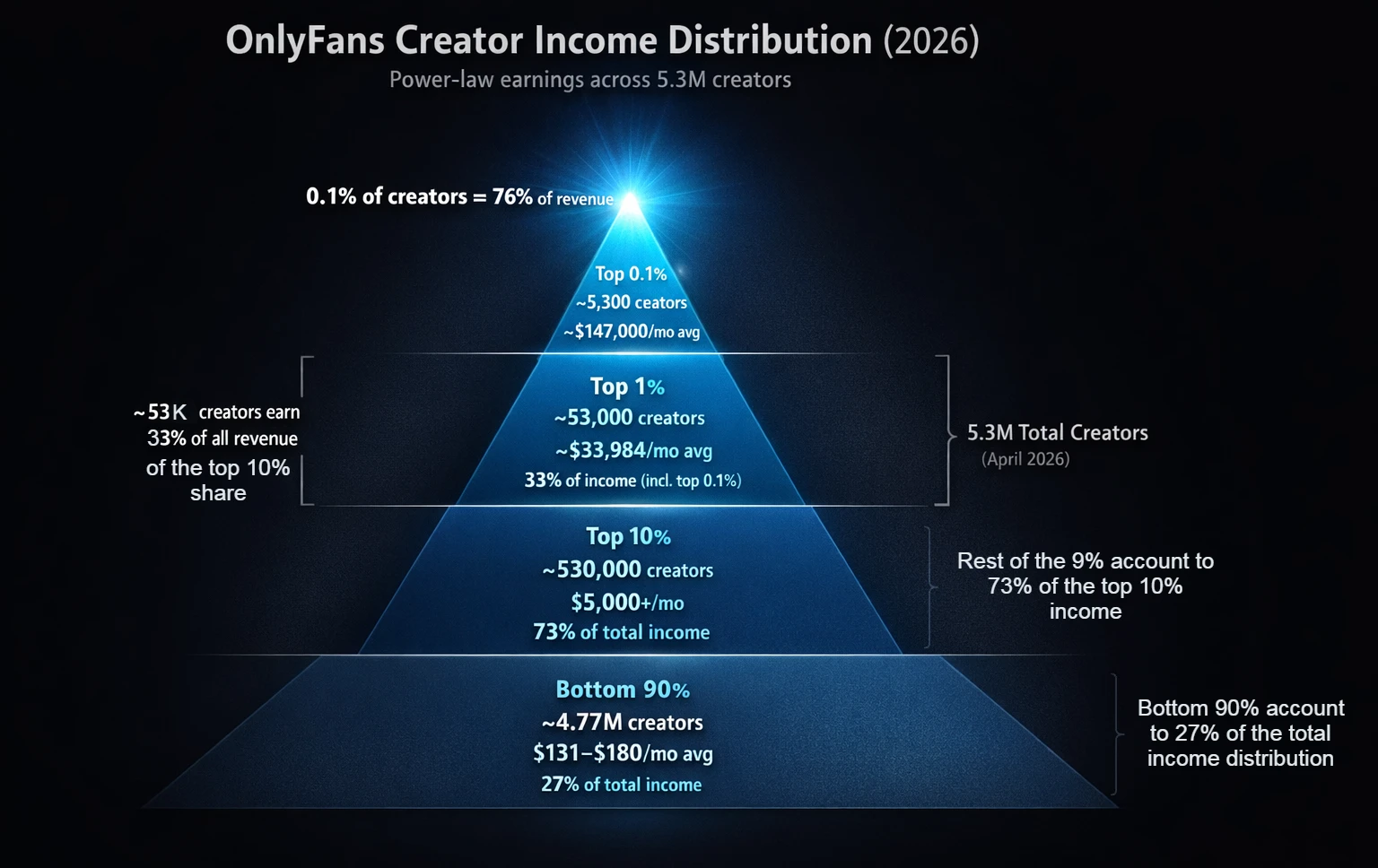

Creator Income Tiers & Distribution

Drilling down into income, the inequality is stark and well-documented. Here is the breakdown using 5.3M total April 2026 creators:

| Creator Tier | Count (April 2026) | Avg Monthly Income | Share of Total Revenue | | --- | --- | --- | --- | | Top 0.1% | ~5300 | ~$147000/mo | 76% | | Top 1% | ~53000 | ~$33984/mo | 33% (incl. top 0.1%) | | Top 10% | ~530000 | $5000+/mo | 73% | | Bottom 90% | ~4.77M | $131–$180/mo | 27% |

This massive skew is sometimes called the "power law" of content platforms. OnlyFans is one of the steepest examples of it across any creator platform globally.

Key Takeaway: Creator earnings follow a power law so extreme that industry commentators consistently warn that "make money on OnlyFans" content is basically fantasy for most people. The bottom 90% of creators (~4.77M people) share just 27% of revenue — averaging under $180/month. This deep inequality is the most important reality check for anyone studying this platform.

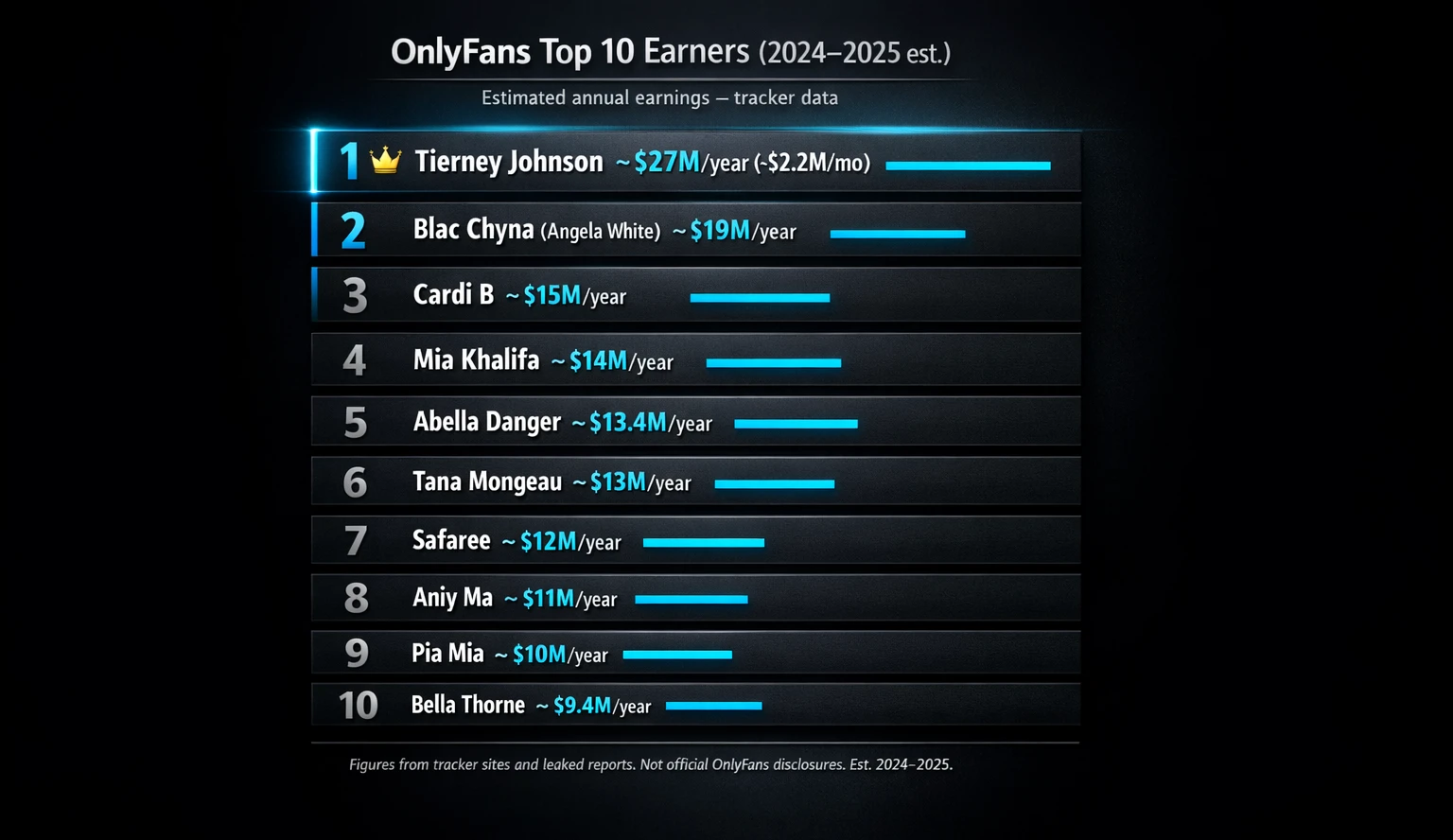

Top Earning Creators

Journalists always want names and figures. Several trackers and leaked reports compile the top earners. For 2024–2025, the highest earners are in the tens of millions annually.

| Rank | Creator | Estimated Annual Earnings | | --- | --- | --- | | 1 | Tierney Johnson | ~$27M/year (~$2.2M/mo) | | 2 | Blac Chyna (Angela White) | ~$19M/year | | 3 | Cardi B | ~$15M/year | | 4 | Mia Khalifa | ~$14M/year | | 5 | Abella Danger | ~$13.4M/year | | 6 | Tana Mongeau | ~$13M/year | | 7 | Safaree | ~$12M/year | | 8 | Aniy Ma | ~$11M/year | | 9 | Pia Mia | ~$10M/year | | 10 | Bella Thorne | ~$9.4M/year |

Note: These figures derive from internal leak reports and specialized trackers, not official OnlyFans filings. They represent best available estimates as of 2024–2025.*

A common pattern: nearly all top earners had massive pre-existing audiences (from music, film, porn, or social media) before joining OnlyFans. Cold-start creators without existing followings rarely reach these levels.

Over **300 OnlyFans creators** have crossed the $1M annual earnings mark — a notable milestone, but still less than 0.006% of all 5.3M creators.

Key Takeaway: The ceiling on OnlyFans is extraordinary — top creators earn over $27M/year. But they are statistical outliers with pre-existing fame and fanbases. The median creator's reality ($131–$180/month) is worlds apart. The top earners attract headlines and backlinks; just make sure your article contextualizes them accurately.

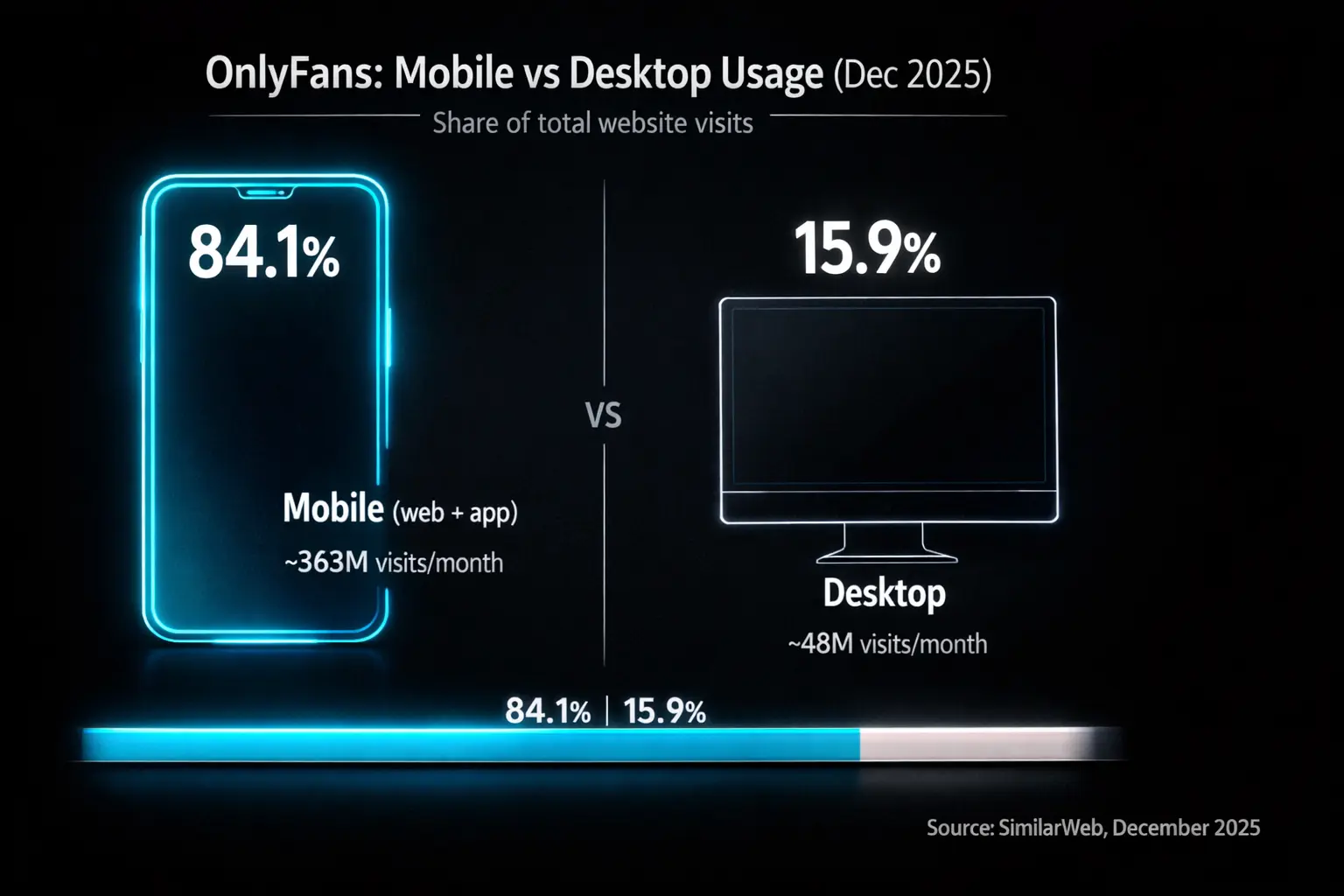

Mobile vs. Desktop Usage

OnlyFans is overwhelmingly a mobile platform. Every analytics source agrees: **84.1% of site visits are on mobile devices**, leaving just **15.9% on desktop** (confirmed December 2025, SimilarWeb). This is a higher mobile share than even YouTube or Instagram.

The implication for creators: assume mobile-first in all content decisions. Videos should be vertical-friendly; text posts optimized for small screens; messaging features easy to use on app. OnlyFans' own product updates consistently prioritize a smooth mobile experience.

Key Takeaway: Almost everyone on OnlyFans is on their phone. Over 8 out of 10 visits are mobile. Creators who optimize for desktop first are optimizing for a 16% minority.

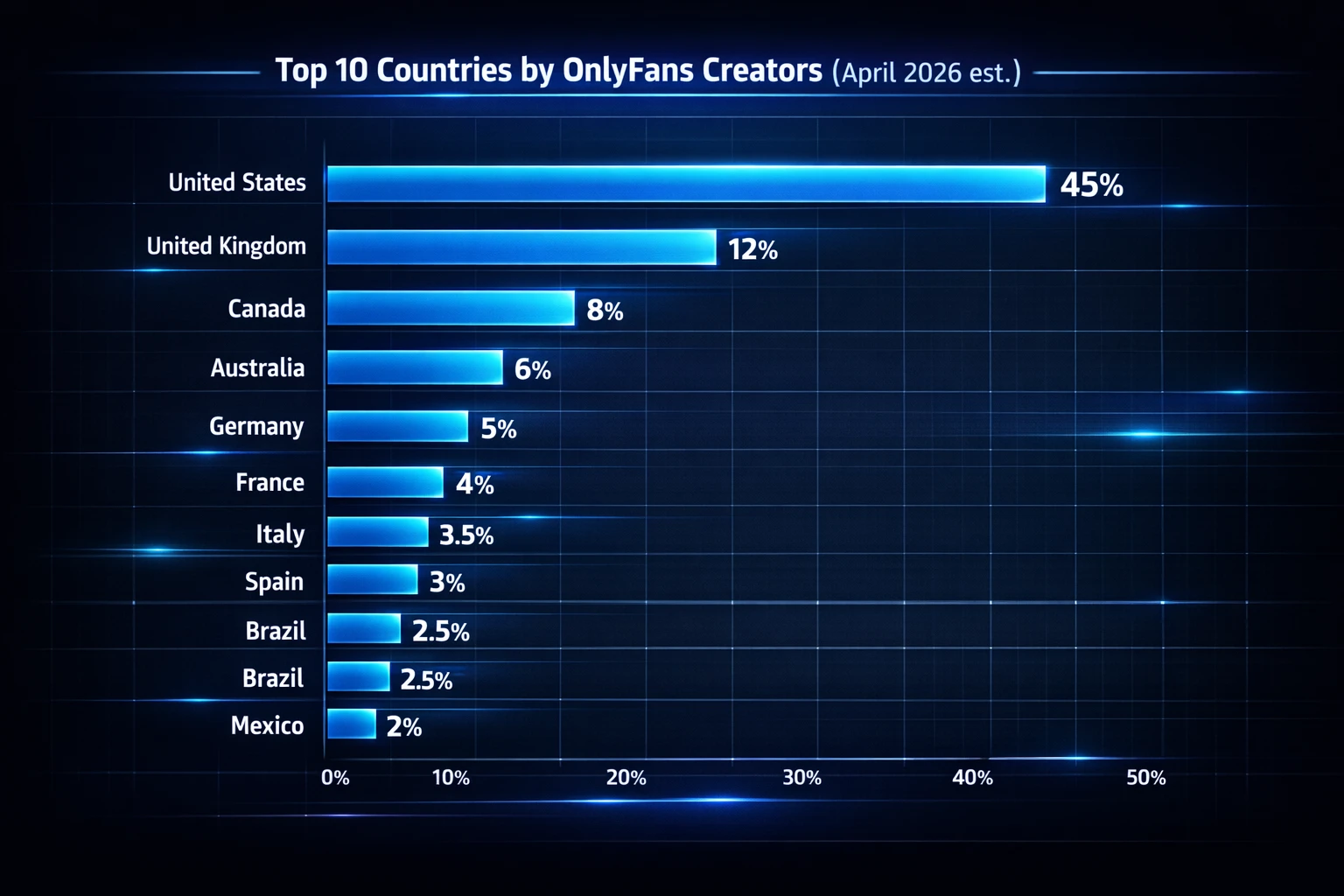

Top Countries by Creators

It's worth distinguishing creator geography from user geography — they tell different stories.

| Rank | Country | Estimated Share of Creators | | --- | --- | --- | | 1 | United States | ~45% (~2.39M creators) | | 2 | United Kingdom | ~20% (~1.06M creators) | | 3 | Canada | ~10% (~530K creators) | | 4 | Australia | ~7% (~371K creators) | | 5 | Germany | ~4% (~212K creators) | | 6 | France | ~3.5% (~186K creators) | | 7 | Italy | ~2.5% (~133K creators) | | 8 | Spain | ~2.5% (~133K creators) | | 9 | Brazil | ~2% (~106K creators) | | 10 | Mexico | ~2% (~106K creators) |

Note: These are directional estimates based on traffic share data and creator community surveys, not official OnlyFans disclosures.

A notable pattern: **Canada produces a disproportionate share of creators** relative to its user traffic share (~10% of creators vs ~4.5% of users) — Canadians punch significantly above their weight on the supply side.

English-speaking countries (US + UK + Canada + Australia) together account for approximately **75%+ of all creators**, reflecting language, payment infrastructure, and cultural acceptance as key enablers.

Key Takeaway: The US is king on both the demand and supply side. But Canada and the UK contribute a larger share of creators relative to their fan base — possibly due to higher cultural acceptance of adult content creation as legitimate income.

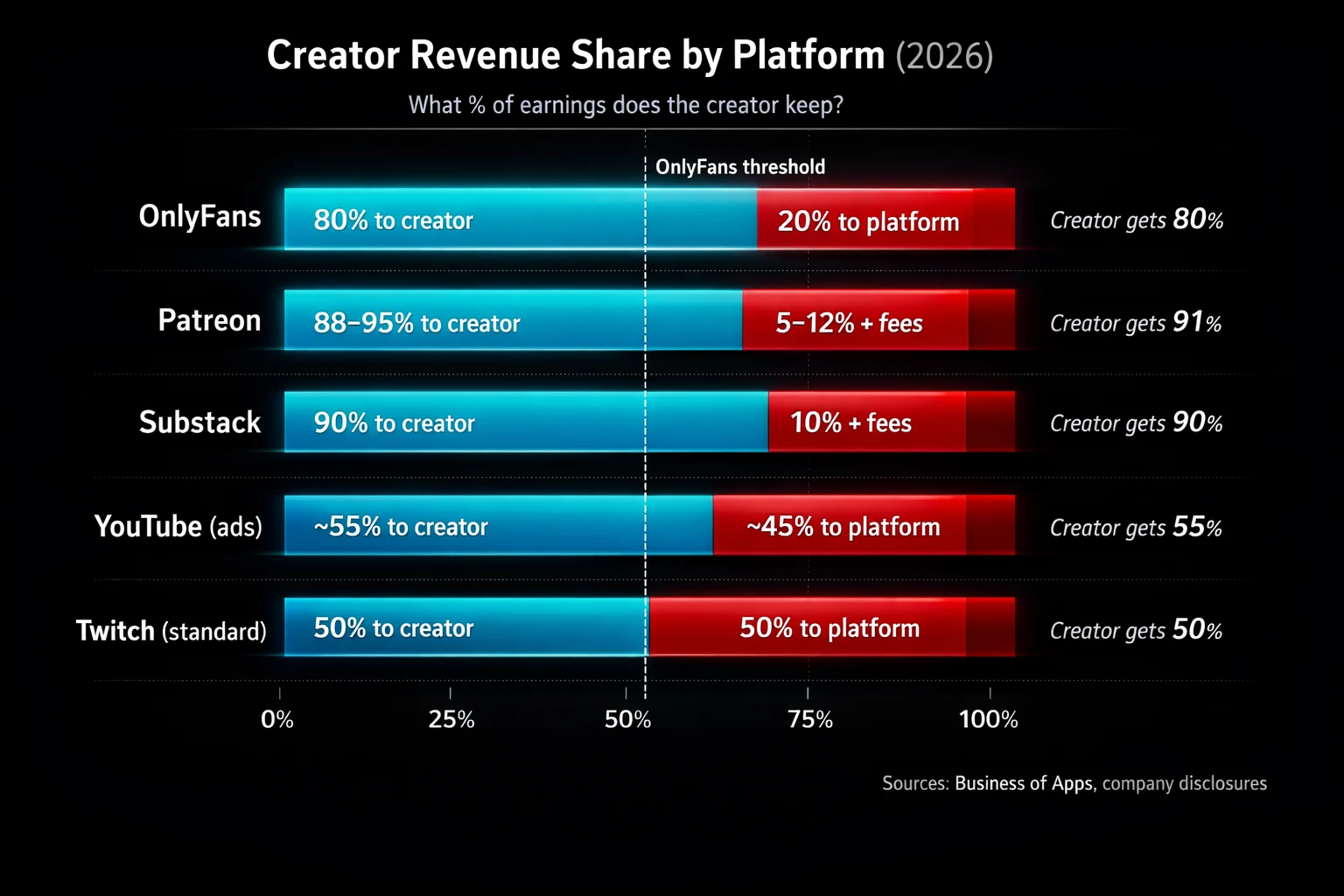

Revenue Share Models

OnlyFans' 80/20 creator split is one of the platform's most-cited competitive advantages. Here's how it compares:

| Platform | Creator Gets | Platform Takes | | --- | --- | --- | | OnlyFans | 80% | 20% | | Patreon | 88–95% | 5–12% + fees | | Substack | 90% | 10% + fees | | YouTube (ads) | ~55% | ~45% | | Twitch (standard) | 50% | 50% |

OnlyFans' 80% is more favorable than ad-supported platforms (YouTube, Twitch) but slightly less favorable than Patreon or Substack in pure percentage terms.

However, the comparison isn't apples-to-apples: Patreon and Substack charge lower % but have far lower absolute earning potential.

An OnlyFans creator earning $10,000/month keeps $8,000. A Patreon creator earning $10,000/month keeps ~$8,800–$9,500 — but far fewer creators reach $10K/month on Patreon.

Key Takeaway: From a creator's viewpoint, OnlyFans' 80/20 split is quite favorable — significantly better than ad-based platforms (YouTube/Twitch) and only slightly behind creator-first tools like Patreon. It's one of the primary structural reasons OnlyFans attracted so many creators and retains them despite growing competition.

Methodology & Sources

Methodology: We compiled the latest data (as of April 2026) from industry reports, financial filings, SimilarWeb analytics, Fanspedia's API, and news sources. Statistics marked (est.) are extrapolated from confirmed 2024–2025 data using published growth rates.

Platform-confirmed figures are cited directly to Reuters, Fenix Int'l filings, SimilarWeb (via Followchain), and PhoeniX Creators' 2026 State of OnlyFans report. OnlyFans does not release real-time public statistics; all April 2026 figures represent best available estimates based on current trajectories.

Primary Sources:

- Business Insider (Fenix International financial filings)

- Reuters (payment volume, creator payouts)

- Wikipedia / Fenix Int'l corporate disclosures (ownership, valuation)

- SimilarWeb via Followchain.org (traffic data, January–February 2026)

- PhoeniX Creators — State of OnlyFans 2026

- Statista (historical user and creator growth)

- DataGlobeHub — OnlyFans Statistics and Insights 2026

- Business of Apps (platform revenue and user benchmarks)

- Official OnlyFans/Fenix press releases and announcements

- Fanspedia's API from 500k + creators in our database

Disclosure: First-person commentary reflects the author's experience as a long-term platform subscriber and observer. Statistical figures are independently sourced and cited. Where ranges exist across sources, we use conservative midpoints and note the variance.

Last updated: April 2026. Next review scheduled: October 2026.